To our Partners at HIT Capital,

HIT Capital’s gain in 2016 was 20% in comparison to the S&P 500’s 12% and Hedge Fund Index’s 6%. This gives HIT Capital a 19% compounded annual growth rate and an overall outperformance of the S&P 500 and Hedge Fund Index by 35% and 79% respectively.

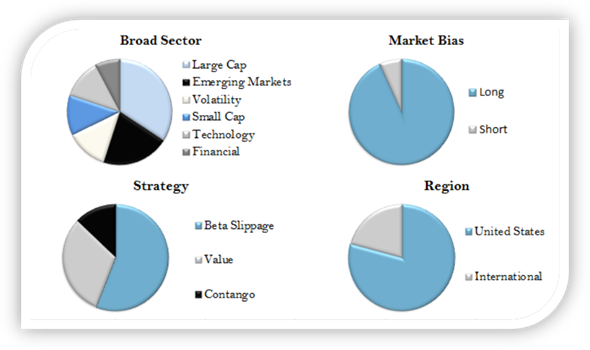

The fund’s outperformance was driven by its primary Beta Slippage strategy. The secondary strategies of Contango and Value also provided positive returns in the latter half of 2016. The Contango premium that evaporated in 2015 came back, earning a return of 68% last year. The fund scored a trifecta with all three strategies outperforming the broader market in 2016.

Mid-year we mentioned the fund’s fundamental value investment in Jones Energy and our expectations that the company would benefit from higher commodity prices. As we hoped, Jones used the depressed market to pick up 18,000 net acres in the Stack and Scoop play in Oklahoma. We believe this area to be the top returning shale play in the USA. In our opinion, the timing was right for Jones to pick up additional acreage at a time of historically low commodity prices but it was not ideal when Jones Energy raised money at a depressed valuation to pay for it. Although we did not appreciate being diluted, we were happy with how and where the capital was spent. Since our investment in Jones Energy on April 12, the stock price increased by 43%. If Jones continues to trend upwards, along with the price of oil, we may close out of the position and pass through our first material capital gain in 2017’ or 2018’.

To ensure that our interests stay aligned with yours, we continue to invest money alongside you. As of January 1, 2016, Stephen Read/HIT Investments own $244k or 17% of HIT Capital. One reason I feel the need to mention this is because of the startling results of Morningstar’s latest report, “Do Managers Eat Their Own Cooking?”. Morningstar found that 47% of investment managers do not invest a dime in their own funds.

As the US market increased in price over the last few years, it did so quicker than the underlying businesses earnings. The US market currently has a Shiller PE of ~26 when historically the average has been around 16. This is one signal that our domestic market has become historically expensive. (The Shiller Price to Earnings ratio is based on inflation adjusted earnings from the previous 10 years)

From a global perspective other markets have not increased at the same rate as the USA and have become relatively cheaper. The United States is now the second most expensive market in terms of Shiller PE, only behind Denmark. In the last quarter of 2016 and continuing into 2017 we plan to increase the fund’s exposure to the cheaper regions of the world when our strategies and associated advantages allow.

Although the United States market becoming more expensive predicts a lower return environment going forward, we will continue to research ways to improve our risk adjusted returns. In the past year we have identified momentum as a possible return-enhancing factor. Using a momentum factor over a one year time horizon has historically provided an advantage over the general market, and when coupled with value it has performed even better. As we become more knowledgeable and confident in the momentum strategy we may start to introduce it into the portfolio.

We thank you for your trust and until next time wish you a safe and prosperous 2017.

Stephen Read

If you received this report through a friend and would like to be added to our semi-annual fund update you can subscribe here.

HIT Capital’s 2017 privacy policy can be found here and Stephen Read’s annual ADV Update is available upon request. If you would like the ADV or privacy policy sent to your inbox please email me at Stephen.Read@HITInvestments.com